The rise in interest rates in the United States has led to adjustments in the technology industry, especially in the United States.

Source: Morningstar Direct, data as of September 30, 2021

Is this correction only a cyclical or a prelude to a more permanent downtrend? It seems difficult to say at this stage because it is based on macroeconomic factors (inflation, Fed policy, China’s situation), but certain basic factors allow us to understand why “technology” has become so important in stock exchanges.

The TMT bubble and its consequences

In the past 30 years, the technology industry has been the engine of profound economic transformation, which has led to a wave of creative destruction (a subject cherished by the economist Joseph Schumpeter) and the emergence of long-term secrets in many fields of activity (Cloud, artificial intelligence, etc.).

Some of these innovations are sometimes based on old concepts brought about by clever marketing discourse, but they have also contributed to the emergence of new careers that contribute to the company’s digital transformation.

This wave of innovation first led to the speculative bubble surrounding Internet stocks in the late 1990s.

After the burst of the “TMT” bubble (2000-2002), new leaders emerged in the technical field, centered on such things as Amazon, Apple, Microsoft, letter (Google) or Facebook with Netflix, Has had a ripple effect on many growth stocks in the media and other fields (Twitter, Break off, Disney), software (Adobe, Sales force, Oracle, intuition, Serve immediately, Autodesk), finance(visa, Paypal, square), Semiconductor (Intel, Nvidia, Broadcom, Texas Instruments, Qualcomm, AMD) Or biotechnology (vertex, Regenerating element, Alexson, Biomarin) And medical technology (Abbott laboratory, Medtronic).

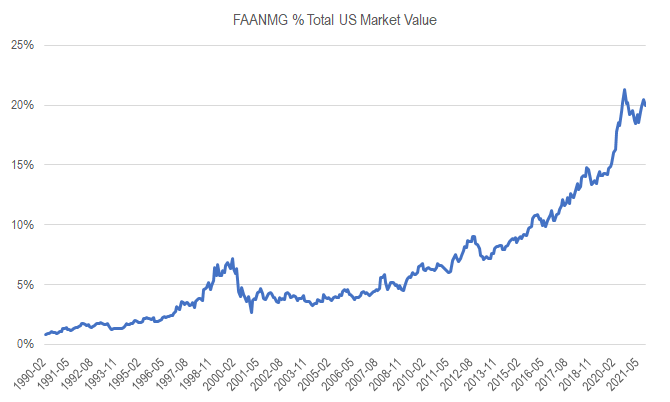

At the same time, there is a concentration effect. These technology giants (“GAFANM” or “FAANMG”) now account for 20% of the US market, compared to 10% and 6% in mid-2015 and early 2010, respectively.

Source: Morningstar Direct, data as of September 30, 2021

Basic explanation

Is there a fundamental reason behind this growing role of technology? Yes. The industry has shown significant profit growth capabilities in the past 20 years.

However, we are reaching the limits of this dynamic because, as Goldman Sachs strategists pointed out in a September 27 study, the top 5 companies in the S&P 500 account for 20% of the index, but only 16% of profit. Morningstar analysts emphasized this point at the beginning of the year.

This shows that the market has shown great confidence in these companies, especially in their ability to maintain a competitive bastion (“moat”), and most importantly, they can continue to outperform their competitors.

However, history shows that for a long period of time, all leaders today are not necessarily able to maintain themselves over time.

Technological breakthrough

There are countless technological breakthroughs.Do we consider the emergence of Salesforce or the recent Snowflake In terms of database management, it has been possible to create new activity parts, making speed a heavyweight in this field, such as Oracle (The founders of Snowflake and Salesforce are both former Oracle employees).

Therefore, the market seems to assume that today’s leaders are likely to remain in this state and will not be “surpassed” by smaller, more innovative companies.

However, the history of the stock market in the past 10-15 years shows that new fields of activity have emerged, which is the result of continuous innovation in the semiconductor industry (computing power and data storage capacity) and communications (transmission speed). New use (network effect).

For example, the coronavirus pandemic has created new demands in telecommuting or hybrid organizations, using “cloud” (cloud computing) more and more, but it has also created new demands in terms of data protection and network security.

Another factor that may cause changes in hierarchical structure and technical weights is regulatory factors.

Around the world, regulators are changing their principles to evaluate innovation not only based on consumer interest (price), but also based on market forces.

© Morningstar, 2021-The information contained in this document is for educational purposes only and is for reference only. It is not intended and should not be regarded as an invitation or encouragement to buy or sell the aforementioned securities. All reviews are the opinions of their authors and should not be regarded as personalized recommendations. The information in this document should not be the only source leading to investment decisions. Before making any investment decision, be sure to contact a financial advisor or financial professional.

.

#Technology #Start #fix

More from Source