The digital transformation of enterprises is a long-term trend, and development is currently accelerating due to the direct consequences of the COVID-19 pandemic. Therefore, careful consideration should be given to the use of this structured and privileged business model to obtain investment opportunities. ServiceNow is rare because it runs a privileged ecosystem business model built into the software. This model has excellent economic benefits and can provide the mission-critical building blocks required by the enterprise, and does not have any meaning today competition.

ServiceNow has enterprise services

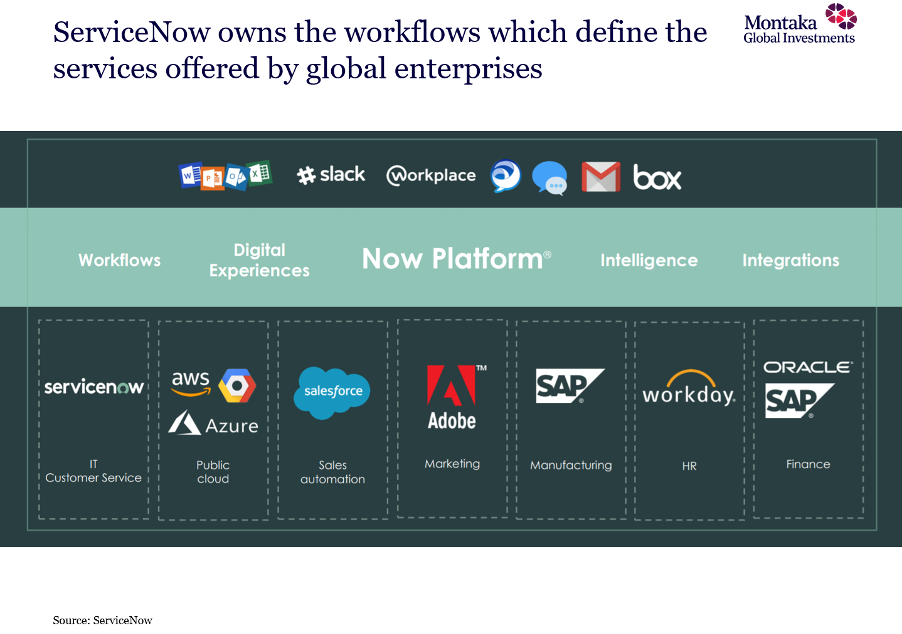

Thinking abstractly, the operation of any enterprise is just a collection of a large number of services. Services usually take the form of human employees interacting with multiple software applications in predefined ways (called workflows).

In most large enterprises, these workflows are defined and delivered by ServiceNow. ServiceNow evaluates, evaluates and optimizes the delivered services. Unlike most software applications, ServiceNow does not attempt to disrupt other enterprise applications. ServiceNow aims to be the “operating system” of the enterprise, enabling employees to deliver services across all functions more efficiently, as shown below.

It is important that all ServiceNow applications (and applications developed by third parties) are built on its Now Platform-a platform that has a single data on the technology stack owned by ServiceNow, from the application layer to its data center model. The infrastructure is distributed all over the world. It is one of the few technology businesses that do not rely on hyperscale cloud providers today.

ServiceNow serves more than 6,000 of the world’s largest companies today, including Goldman Sachs, JPMorgan Chase, Disney and the US State Department. It always provides a best-in-class retention rate of 97%. What’s interesting is that 80% of new customers have new businesses that drive 30% of its annual revenue growth. These new customers come from existing customers because they make fuller use of Now Platform in the entire enterprise’s internal operations.

ServiceNow generates the highest quality cash flow

There are three key reasons why ServiceNow’s cash flow is of the highest quality: (i) ServiceNow’s core workflow products are vital to the enterprise. (Ii) ServiceNow operates without meaningful competition; (iii) The value extracted by ServiceNow is far less than the value added.

To prove the latter, ServiceNow’s largest customer spends approximately US$20 million per year, which is much higher than the average of approximately US$1 million per year for all its customers. But for these big customers, the annual payment of US$20 million to ServiceNow is when the IT budget exceeds US$8 billion!

We believe that the value extracted by ServiceNow is far less than the value added by it. The company also believes this, and points out that for every dollar a customer spends, it can create about $5 in productivity gains. In the context of an estimated potential market of US$165 billion (and the company’s annual revenue is only US$4 billion today), one can see a long room for growth.

ServiceNow’s cash flows are of the highest quality because they are elastic, predictable and growth. From this perspective, the real problem is to question the discount rate applicable to the valuation of such cash flows, especially in the interest rate environment, which is likely to remain close to zero for the foreseeable future.

ServiceNow’s strengths will expand its data

In view of the fact that ServiceNow has full ownership of the Now Platform in the entire technology system, it has a special privileged data set of the world’s largest company, from which it can (and has) developed expected AI-based tools to further enhance the value proposition of its applications for enterprises client.

For example, ServiceNow has only recently introduced AI-enabled virtual agents, predictive intelligence and performance analysis tools in its core IT service management products-80% of new customers have already chosen this higher-value product. But today, the existing customer base still has a penetration rate of only 15%-ServiceNow is confident that this penetration rate will increase to 100% in the next few years.

We strive to have long-term winners in attractive markets. And we believe that ServiceNow is likely to continue to win in enterprise services and workflow in the next few decades.

* * *

Increase your wealth in the long term

Montaka Global Investments provides investors with opportunities to increase wealth in the long run through strict global investment strategies and complex risk management methods. Click “Follow” below to get more insights.

.

#ServiceNow #Mission #Critical #CompetitionAndrew #Macken

More from Source